As Co-Financial Advisor, Estrada Hinojosa & Company assisted the North Texas Tollway Authority (NTTA) with the issuance of $2.5 billion System Revenue and Refunding Bonds, Series 2017A and 2017B. The transaction refunded all outstanding Special Projects System obligations, including a TIFIA loan as well as selected Tollway System debt.

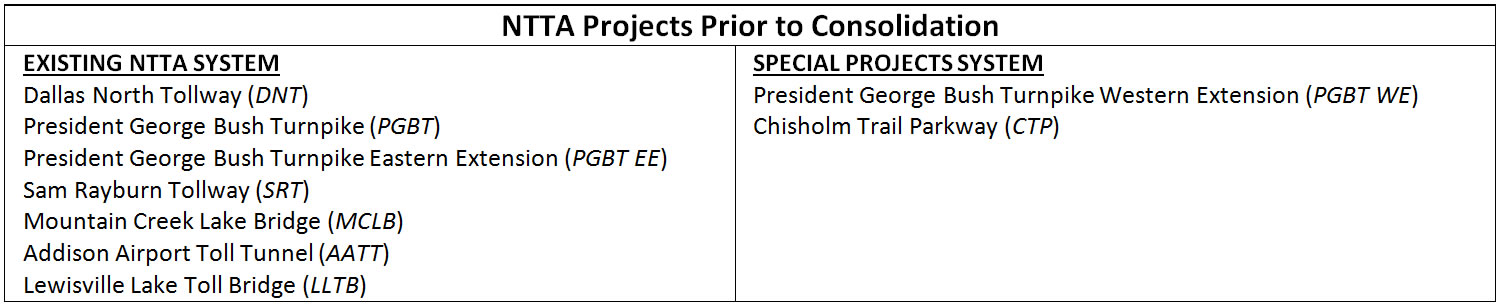

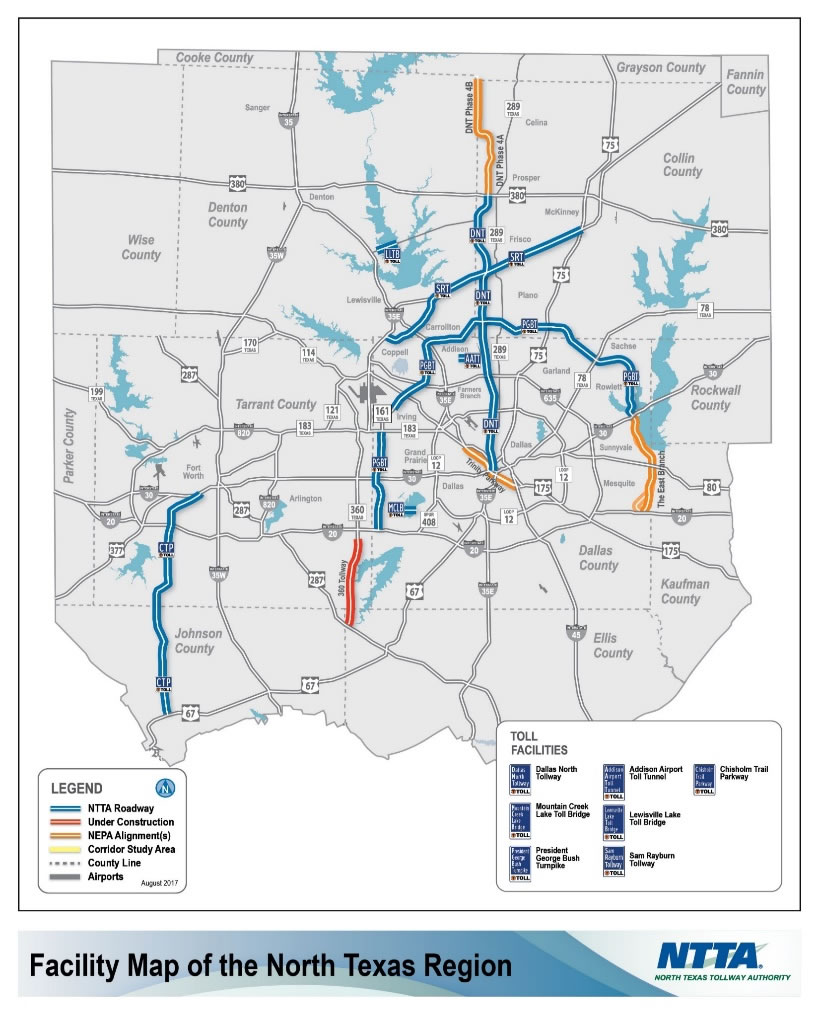

The System and SPS: Prior to this refinancing, the North Texas Tollway Authority administrated two systems that facilitated the financing of seven projects in the DFW Metroplex which have a combined total of 130 center lane miles. In 2011, NTTA issued debt to create a second system, “The Special Projects System”, for two new projects – the President George Bush Turnpike Western Extension and the Chisolm Trail parkway – with 38 center lane miles.

The TELA Agreement: In 2008, NTTA and TxDOT entering into a Toll Equity Loan Agreement (TELA), under which TxDOT made a toll equity loan available to NTTA to provide financial assistance by way of “Credit Support”. The structure of this financial assistance was similar to a “Letter of Credit” and necessitated that the projects be financed, constructed and operated separately and apart from the Existing NTTA System. For this reason, NTTA formed the Special Projects System consisting of PGBT WE and CTP. In 2011, to provide funding for the design and construction of these two facilities, NTTA obtained the $418 million SPS Transportation Infrastructure Finance and Innovation Act (TIFIA) Loan and issued approximately $1.3 billion in bonds secured by the revenues of the Special Projects System.

Under the TELA, if and when certain conditions are met, NTTA agreed to use its good faith efforts to discharge TxDOT of its obligations under the TELA by refinancing the Special Projects System debt without the TELA support. If NTTA was unable to refinance the Special Projects System without the TELA support, the TELA requires NTTA to pay TxDOT an annual TELA fee of over $5 million, beginning in 2022.

Rationale for Refunding: In 2017, NTTA determined that it was economically feasible to accelerate the refinancing of the Special Projects System debt and merge the PGBT WE and CTP assets with the NTTA System because of the higher credit quality. In addition to achieving notable debt service savings, bringing PGBT WE and CTP into the NTTA System would also create efficiencies and reduce operating costs by eliminating duplicate efforts of maintaining two separate systems, including auditing services, budget development, asset inspection, traffic and revenue consultants and financial advisory services.

Plan of Financing: Proceeds from the 2017A and 2017B Bonds were used to refund System Bonds for savings, and refund all Special Project System (SPS) debt obligations onto the System. The structure was unique in that the refunding was split into Senior and Subordinated pieces. The First Tier Bonds were used to refund all of the System bonds for savings and restructure the SPS Series 2011A thru-D. Portions of the 2011D and TIFIA loan were refunded with Second Tier bonds in order to achieve coverage targets. The 2011E (taxable) and portions of the TIFIA loan were refunded with available cash reserves so as to avoid issuing taxable debt. Other aspects of the structure included: 2 Tiers in order to achieve targeted coverage levels

- Various call dates

- Escrow was broken into 3 components

- All tax-exempt

- Bifurcated coupons

- Maximization of funds on hand to defease taxable/make-whole debt

- Use of a surety policy and bond insurance

- Coverage targets (first year only) of 1.70x and 1.40x, growing thereafter

- Savings targets of 5% on System, no loss on SPS with ultimate savings of 14% achieved

Ratings: NTTA conducted on-site rating meeting with Moody’s and S&P. First Tier ratings of A1/A and Second Tier ratings of A2/A- by Moody’s and S&P, respectively, were affirmed due to extensive efforts highlighting the strength of the NTTA System credit, including strong revenue growth, ability to change toll rates at the board’s discretion, history of consistent biennial toll rate increases of 2.7% per year since 2009, a CIP that is on schedule and under budget, strong liquidity and considerably reduced MADS, among many others.

Marketing: NTTA engaged in a 3-day investor tour in which they made 5 presentations. Two were general area luncheons in Boston and New York. The other three presentations were made directly to their top bondholders. In these presentations, NTTA was able to not only speak about the transaction, but also answer any questions that investors had about the System and any concerns. The attendance was overwhelmingly positive, with many of these investors making up the majority of orders placed.

Pricing: The bonds were priced over a two day period – October 11 and 12. The first day was the Retail Order period and the second day, the Institutional pricing. However, the designation policy did allow for professional retail orders to be considered retail for the first day of pricing. The retail order period on October 11 offered priority access to both individual and professional retail investors with demand for certain amounts in select maturities, which generated nearly $2 billion in orders. The institutional pricing the following day, October 12, resulted in an additional $17 billion in priority orders, for total priority orders of over $19 billion across 153 unique investors. Initial coupons were set at 5% with spreads to MMD ranging from 13 to 47bp spread to MMD. For the retail order period, several 2%, 3% and 4% split coupons were added, in addition to two non-callable maturities.

Result: As a result of the overall strength of the subscription (9.2x), NTTA was able to decrease yields by up to 18 basis points in certain maturities on the First Tier bonds and 15 basis points on the Second Tier bonds. The all in TIC was 3.71% on the First Tier Bonds and 3.74% on the Second Tier. Savings from the transaction ultimately resulting in nearly $385 million of NPV savings (14.9% of par refunded).